Three families, of increasing wealth are chosen below as examples.

They each talk with a financial advisor.

Where do they place their money to help them reach their financial goals?

The amounts of money they have to invest:-

- KSh1,000,000

- KSh10,000,000

- KSh200,000,000

Note: The exchange rate where used is KSh110 : 1US$

Example Portfolio- KSh1,000,000

Jim and Jane both work. They are in their late twenties, and they have no children.

They earn approximately KSh50,000 a month each and have KSh1,000,000 left to them by Jim’s grandfather 3 years ago.

In ten year’s time they want to buy an apartment in Nairobi.

Each year their KSh1,000,000 seems to buy less.

Mary, a friend and financial advisor, asks the following:

Emergency cash:

Mary asks them what they would live on if one or both of them lost their jobs?

They say both losing their job at the same time is unlikely.

They decide, however, to have between 1 and 2 months salary in easily accessible cash in case of an emergency.

Medical Insurance:

Do they want to risk their savings on hospital bills?

Jim has a friend who ended up with very high hospital bills from 2 weeks in a hospital’s Intensive Care Unit.

Though they are young and healthy, he said, it would be a good idea to be medically insured.

Life Insurance:

Mary asks if there is anyone dependent on them?

There is no one financially dependent on them so they do not feel the need for Life Insurance at this stage.

Jane says that she does understand the importance of Life Insurance once they have children.

The lump of money received on the death of one or both parents could save their future children from destitution.

Longer term investing and volatility:

Mary asked how much risk are they both willing to take with their investments?

Long term investments that produce a better return will often be bumpier (more volatile).

Jim is quite excited about the possibility of their money building up to KSh2,000,000.

But how will they feel if their investment fall to KSh550,000 during the investment period?

Jane does not like the idea at all. What is the guarantee that the investment will ever come back to 1,000,000/-?

Mary says that many financial institutions as well as ordinary individuals feel that, with a well-diversified choice of good investments, the chances of a satisfactory outcome is worth some risk.

Mary makes the following points:

- She says that it is important to understand there is no guarantee that they will end up with more money at the end of the period than they have at the beginning.

- There is, however, risk to their money in whatever course of action they take.

- If they do not invest, they may not reach their financial goals.

- They are also at risk of their money being eroded by inflation if they do not invest.

- If, however, they are going to panic and sell when their investments fall in value they should only invest in low volatile, albeit low return assets.

- They must understand the level of risk they are willing to take, and how likely they are to get the expected return. Is the expected risk and expected return satisfactory?

Jim and Jane decide to look at the following options:

- A well-situated plot of land near a developing town that they know of. The plot of land may increase in value as the town expands.

- Government T Bills and Bonds for a relatively safe yearly return.

- Two or three well regarded Kenya companies whose shares could be bought on the Kenya stock exchange. Being much higher risk, this might be considered for a smaller portion of their long-term savings, or could be considered in the future when they have saved more money.

Jane and Jim’s final decision for their Portfolio is as below:-

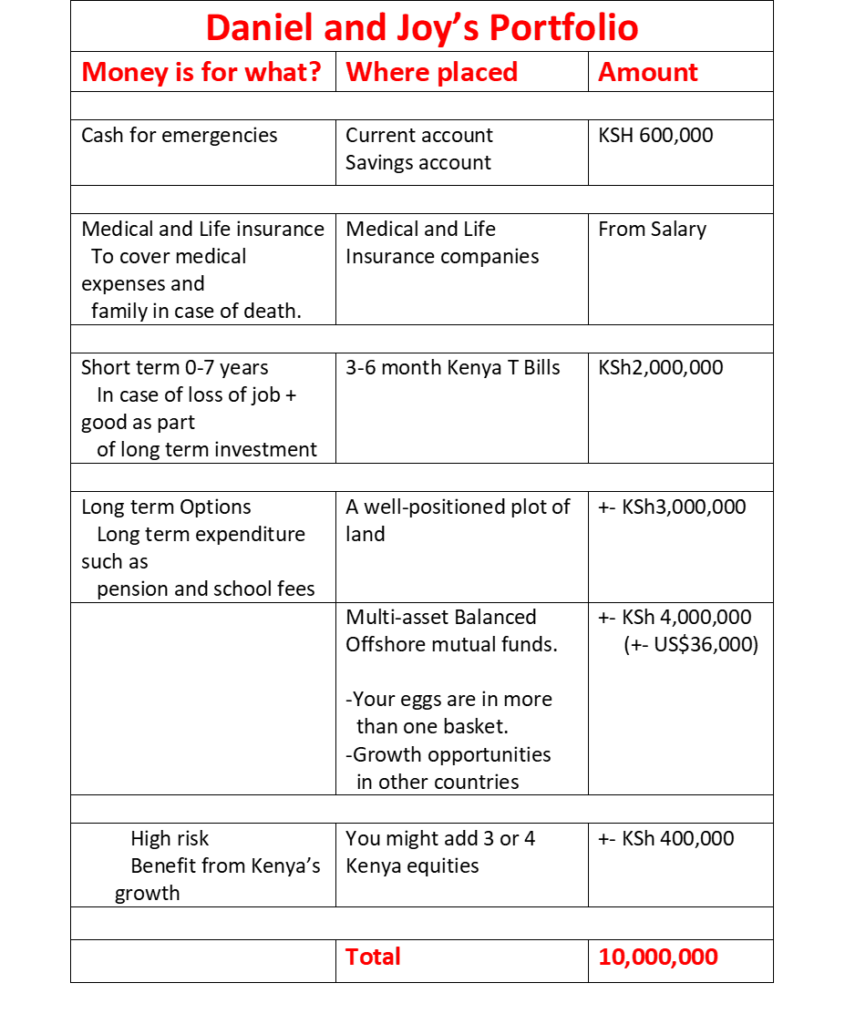

Example Portfolio KSh10,000,000

Daniel, the main income earner, and Joy, both in their forties, have had a good life, spending KSh200,000 a month.

They are now concerned about their retirement in 20 years time.

Through savings plus money from the sale of the land left to them by Joy’s father they estimate they have KSh10,000,000 to put aside for retirement.

Things they need for everyday living seem to be getting more expensive. Will KSh10,000,000 be enough to retire on?

Simon, a retired financial advisor sits them down for a cup of tea. He hasn’t much time but says he can outline a plan of action. This will allow them to think about their future.

They can then speak with a practicing financial advisor who can look after them over the long term.

Emergency and Short term Cash :

Simon asks if they have easily accessible cash available in case of an emergency? What would the family live off if Daniel lost his job and he couldn’t find another job for a year?

- Daniel and Joy decide to build up 3 months’ worth of living expenses and hold this in a bank.

This will come from the savings from their salaries- KSh600,000.

–KSh200,000 they will keep in their current account for easy access.

-KSh400,000 they will keep in a bank savings account, earning a little interest. - It might also be a good idea to buy 3-month and 6-month Kenya Treasury Bills that would come from the KSh10,000,000 for retirement.

They could use this if they had financial problems, but otherwise the money would be a part of their retirement funds.

Simon then says that there are two common financial risks that families face- getting sick and the death or incapacity of the main wealth earner.

Medical Insurance and Life Insurance:

Daniel and Joy explain that they have medical and Life insurance cover.

The medical insurance will go towards covering what can be huge medical bills in the event of sickness or an accident.

If Daniel were to unfortunately die, the life insurance obtained would financially help Joy during a very difficult time.

Longer term investing and volatility:

Simon turns to the long term. He explains to them that there are a number of important factors to take into consideration:

Time frame:

Does the investment suit their time frame?

If they will need the money within the next couple of years, they should be in short term investments. If they don’t need the money for 20 years they can invest in higher risk higher return investments such as equity and property.

Over the longer term they can accept the higher short term volatility that is often associated with higher risk, higher return equity type investments.

Volatility:

Good long-term investments that will grow in value over time will rise and fall in line with the financial markets.

Daniel and Joy must be comfortable with the volatility of good investments that fall in line with the financial markets.

-They will lose a lot of money if they panic and cash in their investments every-time a good investment falls in value.

-If they are liable to panic and sell when their investment loses value they should choose an investment with low volatility, and accept the lower potential return this entails.

-If they can accept a high level of volatility and remain invested if their investments fall in value in line with financial market, they can look for better long term return assets.

Note: Accepting volatility applies to good investments only.

The value of a poor investment will eventually fall as the future value or income flow don’t meet expectation. If the investment managers do not take effective corrective action the value of your investment could fall to zero.

These investments should be avoided.

Diversification:

Daniel and Joy should consider spreading their risks: i.e. diversify their investments into a number of different baskets. If one basket disappears, they will not lose all their money.

In addition, diversification of the assets within the portfolio will reduce the volatility of their total portfolio.

The LESS one asset changes in line with another asset (i.e. the lower the correlation between the assets) the lower the overall volatility of the two assets added together.

They will have the same return with less investment risk.

Institutional and Competence Risks:

A good portion of their money should be:-

-In a well regulated market,

-Held by stable, high credit worthy financial institutions,

-and overseen by competent individuals within these financial institutions.

If this is not the case, you need to be satisfied that the expected return is sufficient to cover the added risk.

Fees:

Be aware of charges.

Example:

If you earn a 10% return and there, is a 15% withholding tax.

You will earn an 8.5% return after tax.

If your institutional fees are 3% this will leave you with 8.5% – 3% = 5.5% increase in your money.

If inflation is 4.5% you are left in your pocket with only a 5.5% – 4.5% = 1% increase in the goods and services your money can actually buy.

If, on the other hand, the institutional fees had been 1% instead of the 3% you would have been left with 3% increase in what you can buy. A very big difference over time.

Option for a Portfolio

Daniel and Joy consider the following as a good option for their portfolio:-

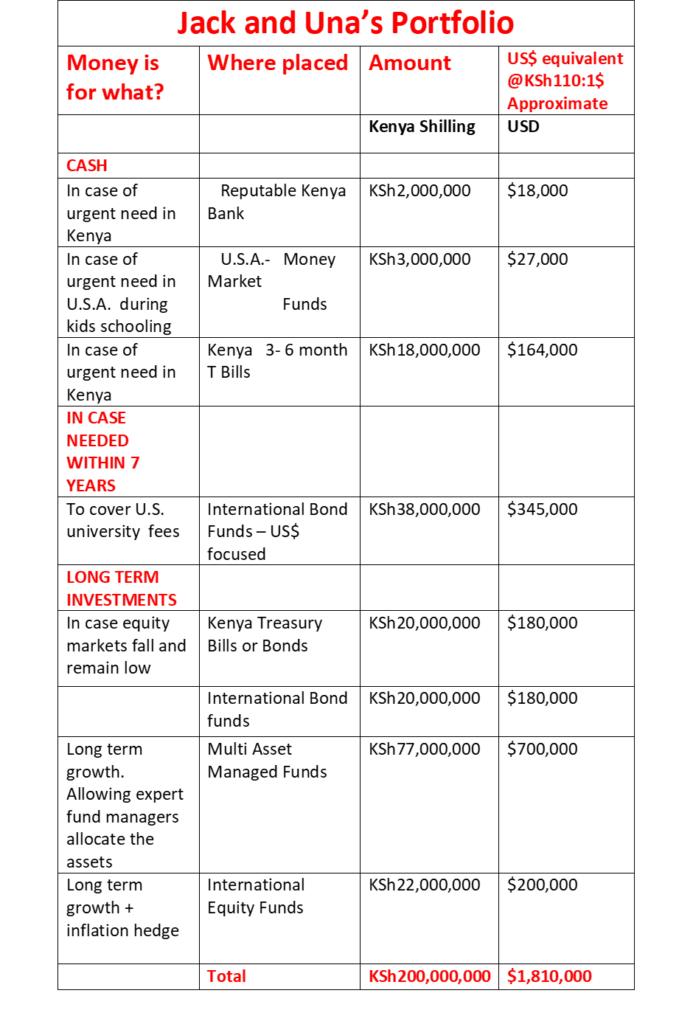

Example Portfolio- KSh200,000,000

How to invest Jack and Una’s KSh 200,000,000

Who are Jack and Una?

Jack and Una are in their mid fifties and live in their own comfortable house within the Nairobi suburbs.

They have two children, Judy and Joseph, who hope to go to college in the U.S. in 3 years time.

Both the parents have had experience dealing with their own finances.

They have built up their wealth from their Kenya property management business which they still operate.

Their net assets (assets less debt) are valued at about KSh 200,000,000 excluding the house they live in and excluding the value of their business. i.e. They have KSh 200,000,000 to invest.

They earn their money from their Real Estate business and their debt is related to their real estate business.

They are approaching retirement, and there is a down turn in the property market. This has worried them.

So much of their wealth is in Real Estate that the down turn in the property market has severly reduced their wealth.

This stimulates them to reassess their finances.

“Where should their money be invested?”

Their Children Judy and Joseph:-

Though Jack and Una want to remain in Kenya the family is internationally orientated.

Their daughter, Judy, is starting a 4 year U.S. university course in 3 years time.

At the same time, their son, Joseph, will be starting, on a 3 year course at a different university but also in the USA, and also in 3 years time.

Andrew, the financial advisor:

To help them pull their ideas together and formulate a strategy they meet with Andrew, an independent financial advisor.

Andrew, the financial advisor, is married and about to retire.

He has seen the good times and the bad times. He is a wise old man.

He has seen people build a comfortable life style for their family over a life time of saving.

He has also seen people become wealthy through success and/or luck, and THEN for this wealth to seep away into the sand.

Andrew takes down all the details required to enable him to give them good advice.

He goes through important first steps:

-Have they an up to dated Will? – They definitely should have.

-Have they medical insurance? – They should have.

-Do they need Life insurance? – Possibly but not necessarily given their wealth.

Andrew then divides their investment requirements into three time frames:

- Easily accessible money, e.g. for emergencies.

- Money they need to use within 7 years, e.g. for university fees .

- Money they will need in the long term, e.g. for retirement.

Easily accessible assets :

Cash available in Kenya

They need cash for business debt repayments. This presently comes from their business rental income.

If there is a problem in the Kenya rental market they could find that they can’t get the cash to cover their debt payments.

They would need another source of cash to cover any shortfall in rental income during this difficult period.

Given how volatile the rental market can be Andrew suggests they have KSh 20,000,000 available to be drawn upon at a moment’s notice.

- KSh 2,000,000 will be in a current account and a savings account, with a major bank.

They will earn a little interest from the savings account and have nearly immediate access to it.

- KSh 18,000,000 they have split into two separate 6 month T Bills. They get a higher return for 6 month T Bills than they do for 3 month T Bills.

They stagger the investment into the two T Bills. They will then have only 3 months before they can access some of the investment should they need to.

For example:

The first T Bill they invest on 1st January will mature and will be rolled over(reinvested) into a new 6 month T Bill on 1st July .

The second 6 month T Bill will be invested 3 months later than the first T Bill, i.e. on the 1st April and so will mature and be rolled over 6 months later than the first i.e. 1st October.

Thus KSh 9,000,000 will be available, if need be, every 3 months from one of the maturing 6 month T Bills.

Added to this KSh 2,000,000 will be immediately accessible from their bank current account and savings.

The Kenya T Bills will earn a return that after tax will approximately cover inflation.

The Bank savings account will probably give interest after tax of less than inflation, but money in the bank has the benefit of being easily and immediately accessible.

Emergency money- USA

In addition an emergency could arise in the USA involving one of their children while studying. They want to hold the equivalent of $30,000 (KSh3,300,000) in a US based money market fund, which will give them immediate access if need be.

Total amount in easily accessible money in both Kenya and the USA = KSh23,300,000 (Approximately US$ 210,000)

Investments for with-drawl within 7 years:

Jack and Una’s prime concern for these years are the educational fees for Judy and Joseph. They need to take into account inflation when calculating their children’s future school fees.

Calculating future college fees:

Historically they note that university fees have increased by 5% a year.

They calculate as follows:

– Present cost- $40,000

Multiplying each year by the expected inflation rate of 5%+1=1.05

– In 1 year’s time the fees will cost- 1.05 x $40,000 = $42,000

– 2 year’s time- 1.05 x $42,000 = $44,100

– 3 year’s time- 1.05 x $44,000 = $46,305. So for 2 children 2 x 46,305 = $92,610

– 4 year’s time- 1.05 x $46,305 = $48,620. For 2 children 2 x 48,620 = $97,240

– 5 year’s time- 1.05 x $48,620 = $51,051. For 2 children 2 x 51,051 = $102,102

– 6 year’s time- 1.05 x $51,051 = $53,604. For 1 child 1 x 53,604 = $53,604

Total school fees will be approximately = US$345,000 ($92,610+97,240+102,102+53,604)

i.e. KSh37,950,000 (KSh110 :1$)

These are the years the children will be at university.

University fees:

They have calculated they will be spending KSh35,200,000 ($345,000) on university fees within 7 years.

If they are paying in Kenya Shilling, and the shilling falls in value against the US$, this will result in the need for more Kenya shillings to pay the fees.

To avoid this risk the money for university fees will be denominated in US$.

If they were conservative this money could be held in a mutual fund holding short dated sovereign debt.

Joseph and Judy decide, however, because of the large size of their over-all wealth, they can include higher risk higher return ‘High-Yield Debt’ within their medium-term portfolio.

Thus they will invest in a spectrum of debt that includes this more conservative Sovereign Debt as well as High Yield Debt.

To somewhat reduce the higher risk of High Yield Bonds, this money will be invested through an established financial institution with a reputation for good fund managers such as PIMCO and Dodge and Cox.

Note: High Yield Debt can include non-developed nation debt as well as corporate debt. There is the probability of a higher return, but with a higher risk of default than sovereign debt.

Higher yield debt is usually less volatile than equities.

Additional Fixed Interest Debt:

Why Invest in additional Bonds:

Both Jack and Una are nervous that the world and Kenya have the potential for change.

This change may create the need to access a large amount of money within 7 years in addition to their children’s university fees.

This could come at a time when there is a precipitous and sustained fall in value of the equity markets.

Thus they decide to add more fixed interest debt.

Their Bond investment will be less volatile than their long term investments that will include equities.

They are willing to accept the potentially lower long-term returns to avoid the possibility of selling equities when the markets have crashed.

How much additional money should they put in lower risk, but lower return investments such as Bonds?

Presently they have made a decision on:-

Cash- $210,000 (KSh23,100,000)

Bonds for School fees- $345,000 (KSh35,200,000)

They are near retirement.

Historically there are periods when stock prices have fallen and stayed low for extended periods of 10 years or more.

If so, having money in bonds will reduce the impact on their portfolio should they unexpectedly need a lump of money.

They can cash in the bonds rather than the devalued equities.

They decide to place a further $360,000 (KSh40,000,000) in bond funds.

A portion will be invested in the more conservative Sovereign Debt bonds.

In an emergency if at a time the stock markets have fallen the Sovereign Debt will be the first to be cashed in.

A portion will be invested in High Yield bonds. In difficult times these will probably fall in value more the the Soveriegn debt funds, but less than equities. These will be the second asset type to be cashed in.

Hopefully they will be able to leave the equities to remain invested. These can then increase in value again when the good times return.

Kenya T Bills/Bonds:

Of the $360,000 of additional money they want to invest in bonds, approximately $180,000 (approximately KSh20,000,000) will be invested in Kenya government 6month to 2 year T Bills.

This gives them a bit of padding in case they need the money to be situated in Kenya.

Why should the money be kept in Kenya?

Though very unlikely, capital controls and restrictions on the movement of foreign currency could be placed on Kenya.

International Bonds:

The remaining $180,000 (KSh20,000,000) they will be invested overseas in a mix of conservative sovereign debt and High Yield bonds.

Being invested in the international financial markets increases the investment opportunities.

It also reduces the risk of being solely focused on a single economic unit, Kenya.

In addition, the diversification will also reduce the volatility of the whole portfolio.

Longer term investments:

Of Jack and Una’s initial KSh200,000,000, they have KSh100,000,000 ($909,000) left to invest.

They have so far invested KSh100,000,000 ($909,000) in short term investments.

KSh100,000,000 is left to be invested for the long term.

Investing in Managed Multi Asset funds and Equities:

Jack and Una expect the remaining KSh100,000,000 ($909,000) they expect to grow over the long term, but with acceptable risk. It is for them when they grow old, and for them to pass on to their children.

Good multi-asset funds and good equity funds have produced long term growth in the past.

Multi Asset Funds:

Andrew, has explained to them that Asset allocation is one of the most important aspects of their portfolio.

Note: Asset allocation is splitting your money up and investing in different things. These assets you end up with might be 40% in Equities, 20% in Bonds, 20% in Property, 10% in Alternative Investments and 10% in Cash.

Jack and Una, though a smart couple, have little experience investing in the international financial markets.

Given the importance of Asset Allocation they decide to depend upon a good fund manager from a reputable firm to manage 70% of the 100,000,000/- .

The funds could include equities, bonds, property, commodities, hedge funds etc.

The benefit of investing through a Multi asset managed fund is that they will have skilled fund managers deciding how much to invest in what.

For example, if world equities look over valued at a point in time, the fund manager can reduce their investment in equites and transfer the money into other asset classes that look more hopeful.

Equity Funds:

For the higher growth but higher risk portion of their portfolio they will invest KSh30,000,000 ($270,000) into equity funds.

They accept that equities are more volatile than are cash and bonds.

However they have higher growth potential.

Jack wants the potential for this higher growth.

Hedge against inflation: Inflation can eat away at the ‘real’ value of bonds and cash.

Equities will be somewhat of a hedge against inflation. Successful companies can increase the price of their products to keep up with inflation, and so may act as a hedge against inflation.

Again, to mitigate the risk, they will invest through well regarded fund managers working with reputable financial institutions.

So Jack and Una end up with:-

Cash for liquidity- easy to get hold of.

Bonds for security in case of equity market turbulence.

They will give a little growth to cover costs and hopefully a little bit more.

Equities to grow their money over the long term and to hedge against inflation.

Home

Important: This information on this WEB site ALONE should not be used to make investment decisions. Investing is particularly personal and is dependent upon your circumstances. You are strongly advised to take independent expert advice before deciding whether to/ or whether not to invest your money.