Why make a budget?

You can save for those things that are really important.

A budget will allow you to decide what you want to spend your money on and what items to save on.

A budget is a road map to show you how to reach your financial goals.

Sections Below:-

Jack’s usual spending:

Jack’s Budget:

Now do this for yourself:

Can’t seem to save:

For many of us, we know what we want and when. We know how much we need to have to get us there. We know how much we make.

But……..we spend all our money. We helplessly ask ourselves: “where are we going to get our savings from?”

The answer is to make a budget for yourself.

A budget allows you-

- To look at what money you have,

- To look at what you spend this on, and then

- To be able to reduce your spending on those things that are less important to you so that you have money left over to spend on the important stuff.

Example:

Jack has a business he started.

He is doing really well with his business but he is tired and needs to splurge money on a holiday. At the same time he must build up enough money for his daughter’s (Sally’s) school fees. He is making, on average 200,000/- per month after tax, but he doesn’t seem to have anything left over at the end of the month. What is he to do?

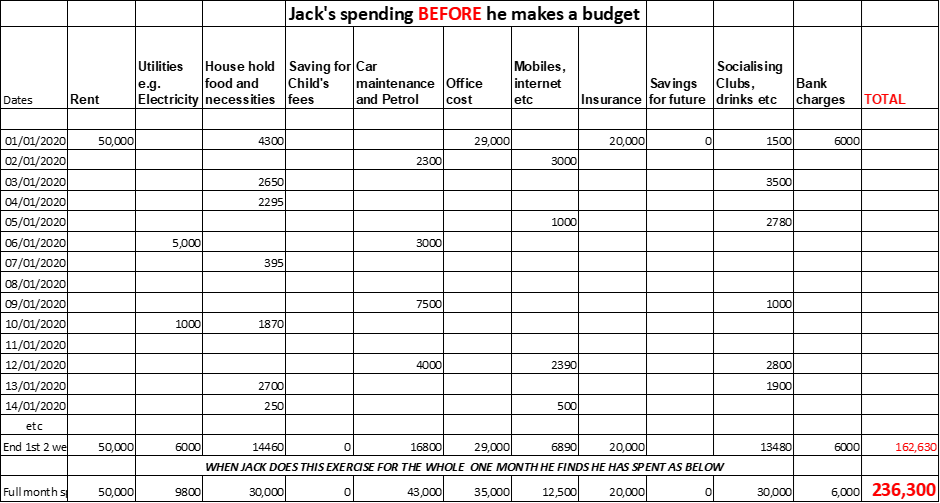

Jack’s usual spending:

Jack makes a list of the main items that he spends his money on every month. He writes these into an excel spread sheet columns-see below.

Each day he writes down what he has spent that day into the correct column.

He adds up each column at the end of each month. Over time he can see where he is spending his money.

Below I have shown how to add in your costs on a daily basis for only 2 weeks so it easy to see.

You should do this for the full month.

Jack fills in his daily expenditure for the full month and finds he is spending KSh236,300.

Note Jack is spending 236,300/- while he is earning an average of 200,000/- a month. He is probably using expensive credit cards or an expensive bank over-draft. You can see this from the 6000/- bank interest charge, indicated under Bank Charges.

He clearly sees that he is not spending or saving on two things that are important for him- Sally’s education and a holiday.

He also sees that there is spending that he could comfortably cut back on.

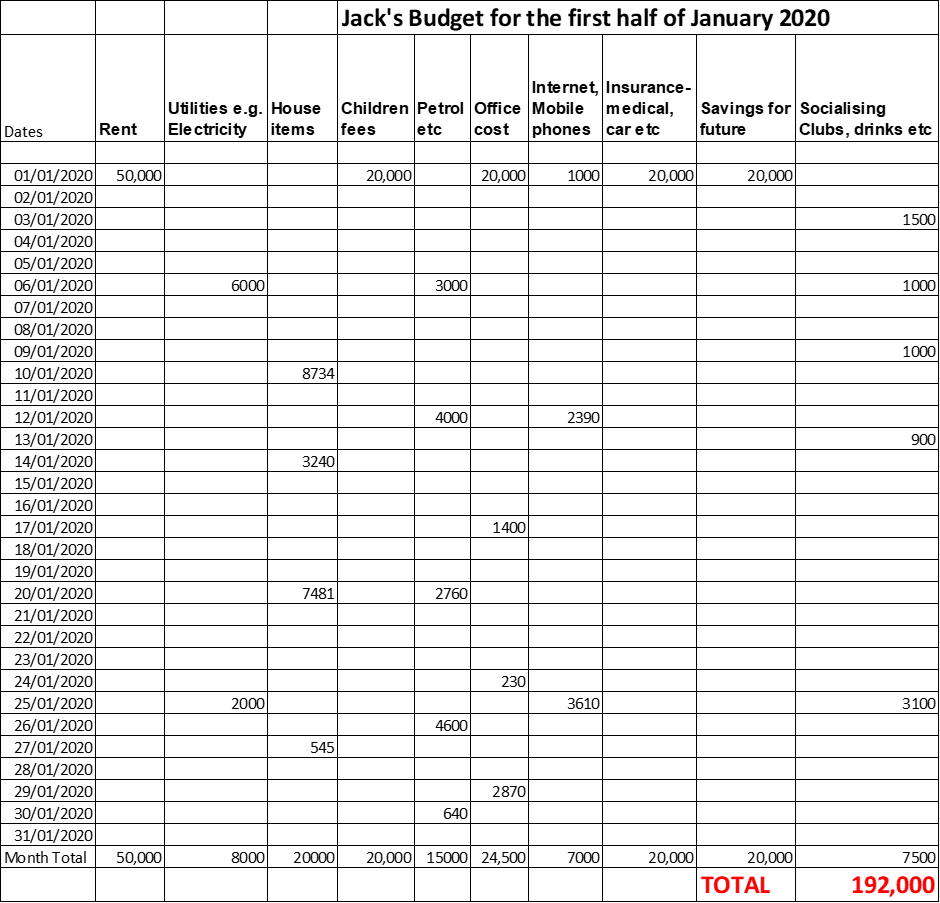

Jack’s Budget:

He puts together a budget. The budget is what he PLANS to spend. This will allow him to save for Sally’s education as well as the holidays that will allow him to recharge his batteries.

Jack will try to spend only what he has planned for in this budget.

Note he has reduced his spending and so is able to stop using his credit card, saving himself an unnecessary expense.

Now do this for yourself:

How does your spending relate to your priority items?

Are you saving enough?

A couple of hints when accounting for your spending and making adjustments:

- Debt will often cost you more than you can make from your investments.

Debt is usually a definite amount each month.

While investments may or may not make you a return.

So, unless interest on debt is much lower than the return you expect from investing you might consider getting rid of this debt. - Keep a daily tab of your spending. Day old information is easy to remember and so it is little hassle to keep your records up to date.

- Be honest with yourself.

- Include all your spending.

- A ‘want’ is not a ‘need’. You can cut back on ‘wants’!

- Make sure you have a column for having fun, as well as a column for savings.

Now that you are saving you will begin to build a lump of money.

Investing: Leave it under your mattress and it will be eaten by inflation. It is time for you to think about investing your savings and make them work for you.

I’ve got money!- Now what?

Important: This information on this WEB site ALONE should not be used to make investment decisions. Investing is particularly personal and is dependent upon your circumstances. You are strongly advised to take independent expert advice before deciding whether to/ or whether not to invest your money.